Want to know how much your money can grow over time? I remember when I first started thinking about my future. I had $500 in my bank account and no idea what to do with it. That’s when I found my first investment calculator. It changed how I think about money.

Investment calculators are simple tools that help you see your money’s future. They show you how much you can earn if you start saving today. You don’t need to be good at math. You just need to know a few basic things about your money.

These tools help you make smart choices. They answer questions like: How much should I save each month? When can I retire? Will I have enough money for my kids’ college? Let me walk you through everything you need to know.

What Is an Investment Calculator

An investment calculator is a simple online tool that helps you see how your money grows. Think of it like a crystal ball for your savings. You put in some numbers, and it shows you what might happen to your money in the future. You tell it how much you have now, how much you plan to add each month, and how long you want to save.

Then it shows you the total amount you could have. I use these tools all the time. Last year, I wanted to save for a new car. I put my numbers into a calculator. It showed me I needed to save $300 every month for two years. That was way more clear than just guessing. The best part? These calculators are free. You can find them on bank websites, money apps, and finance sites. They take less than two minutes to use.

According to data from the Securities and Exchange Commission, investment planning tools help people make better money decisions. When you can see your future savings in real numbers, you’re more likely to stick to your plan.

How Investment Calculators Work

Investment calculators use a simple math formula to show you future money.You give the calculator four main things: your starting money, how much you add each month, how many years you’ll save, and what return rate you expect. The calculator then uses compound interest to show your future total.

Let me break this down. Say you start with $1,000. You add $100 every month. You save for 10 years. The calculator assumes your money grows at about 7% each year. After 10 years, you won’t just have the money you put in. You’ll have extra money from growth. The magic here is compound interest. That’s when your money makes money, and then that new money also makes money. It’s like a snowball rolling down a hill, getting bigger and bigger.

The Compound Interest Calculator can show you exactly how this snowball effect works. You can play with different numbers to see how small changes make big differences over time.

Types of Investment Calculators You Should Know

Different calculators help with different money goals. Let me show you the main ones.

- Retirement calculators help you figure out how much to save for when you stop working. You tell it your age, when you want to retire, and how much money you spend each year. It shows if you’re saving enough.

- College savings calculators help parents plan for their kids’ education. My friend Sarah used one when her daughter was born. It told her she needed to save $250 per month. Now her daughter is 10, and Sarah is right on track.

- General investment calculators work for any goal. Want to save for a house? A vacation? A new business? These tools show you the path. They’re the most flexible type.

The Future Value Calculator is great for seeing what any amount of money could become. You can try different saving amounts to find what fits your budget.

Key Numbers You Need for Any Investment Calculator

Every calculator asks for the same basic information. Here’s what you need to know.

- Your starting amount is how much money you have right now. This could be $50 or $5,000. Any amount works. Don’t worry if it’s small. The important thing is to start.

- Monthly additions are how much you plan to save each month. Be realistic here. I once told a calculator I’d save $500 per month, but I could only really do $200. The calculator was useless because I lied to it.

- Time period is how many years you’ll save. Most people use 10, 20, or 30 years. The longer you save, the more your money grows.

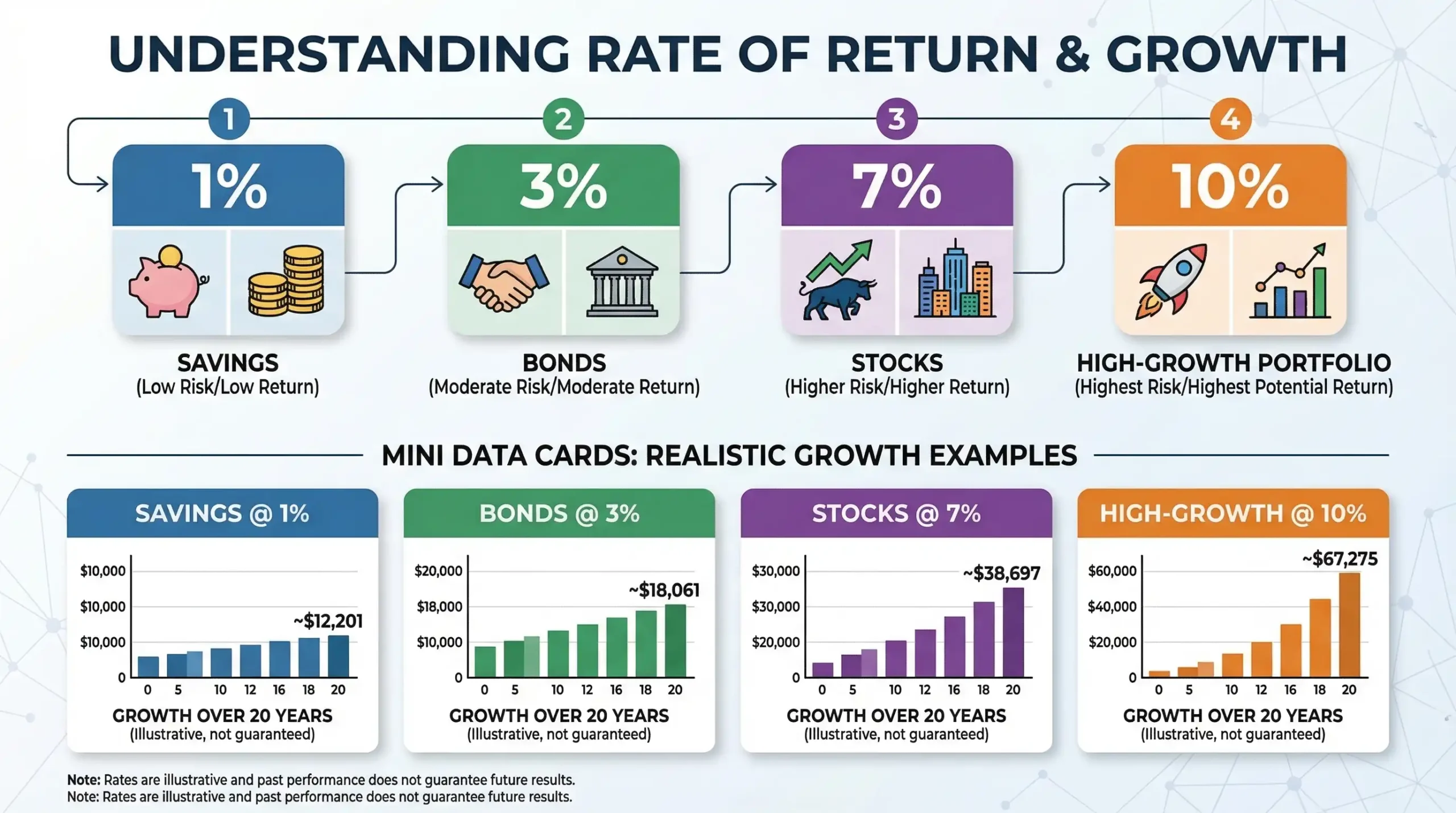

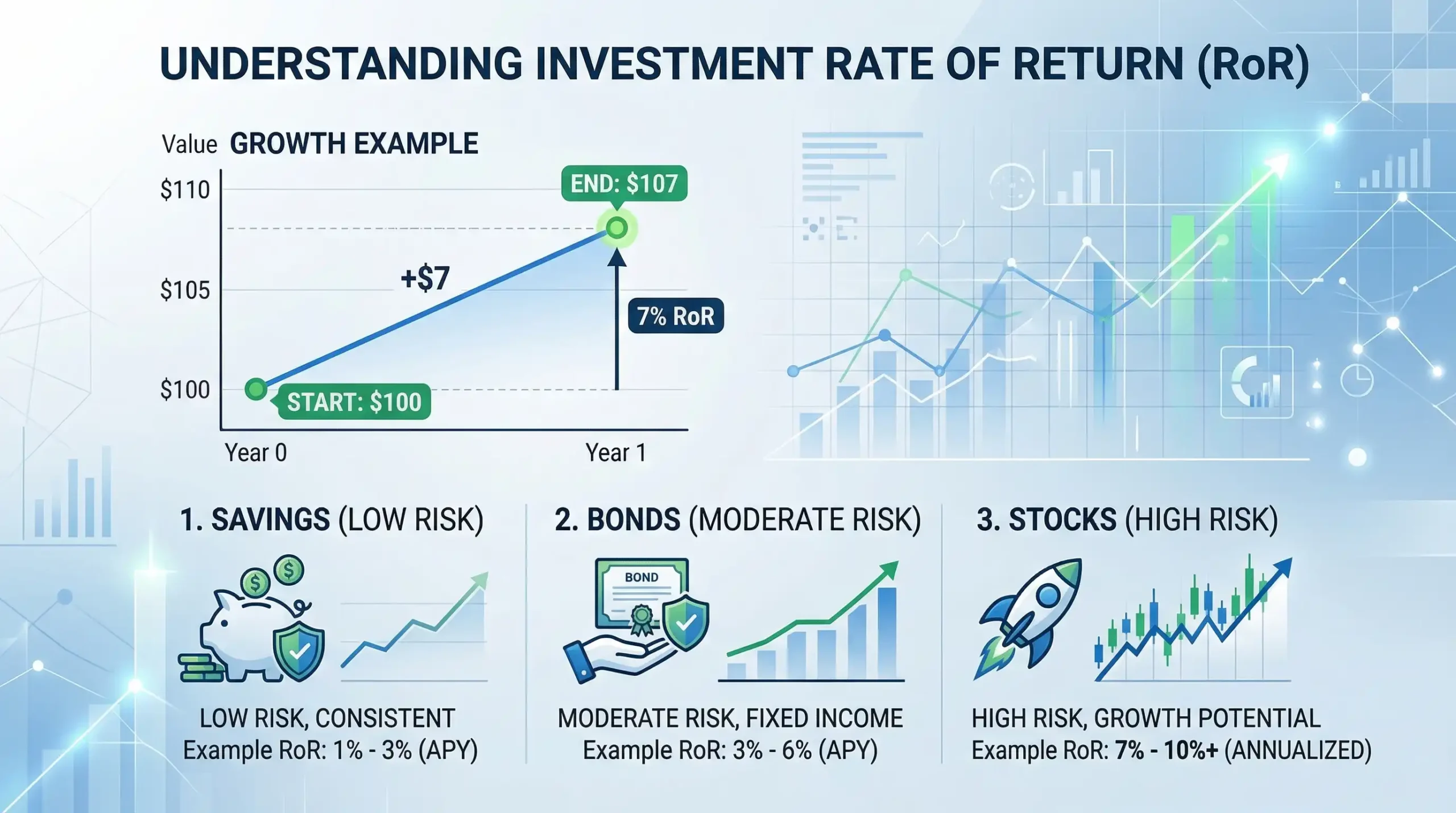

- Rate of return is how much your investment grows each year. Stocks have grown about 10% per year over the last 50 years, according to research from Standard & Poor’s 500 index data. But past results don’t promise future returns. Most calculators use 5-8% to be safe.

Understanding Rate of Return in Simple Terms

The rate of return is just how fast your money grows each year. If you put $100 in a piggy bank, you still have $100 next year. That’s a 0% return. But if you invest that $100 and it becomes $107 in one year, you got a 7% return. Different investments give different returns.

Savings accounts give about 1-2% right now. Bonds give about 3-5%. Stocks have given about 10% over many years, but they go up and down a lot. Here’s something I learned the hard way: higher returns usually mean higher risk. My cousin put all his money in a stock that promised 20% returns.

He lost half his money when that company went down. Slow and steady usually wins. Most financial experts suggest using 6-7% for your calculator if you’re investing in a mix of stocks and bonds. This is conservative, which means it’s safer to plan with lower numbers.

Common Mistakes People Make with Investment Calculators

I’ve made almost every mistake possible with these tools. Let me save you the trouble.

- Being too optimistic is the biggest error. People put in 12% returns because they heard stocks can do that. But real life is messy. Markets go down sometimes. Use realistic numbers like 6-7%.

- Forgetting about taxes is another big one. If your calculator says you’ll have $100,000, you might actually have less after taxes. Some investment accounts like Roth IRAs don’t get taxed, but regular accounts do.

- Not updating your numbers is something I do all the time. Your life changes. You get a raise. You have a baby. You buy a house. Go back to your calculator every year and put in new numbers.

- Ignoring inflation makes your future money look bigger than it really is. A study from the U.S. Bureau of Labor Statistics shows that inflation makes money worth about 3% less each year. What costs $100 today might cost $130 in 10 years.

Investment Calculators for Different Life Stages

Your money needs change as you get older. Different calculators help at different times.

- In your 20s, you’re just starting out. You might not have much money, but you have lots of time. Time is actually more valuable than money at this age. Even $50 per month can grow into a large amount over 40 years.

- In your 30s and 40s, you’re probably thinking about buying a house, having kids, or starting a business. Use calculators to balance multiple goals. I’m in this stage now, and I use three different calculators for three different goals.

- In your 50s and 60s, retirement is getting close. You need more accurate numbers. Update your calculator every few months. Make sure you’re saving enough.

The Stock Average Calculator helps if you’re buying stocks over time. It shows your average price and helps you make smart buying choices.

Dividend Investment Calculators Explained

Some investments pay you money just for owning them. These are called dividends, and special calculators help you track them. A dividend is like rent payment from a company. You own a piece of the company through stocks, and they pay you part of their profits. Some companies pay these every three months. I started getting dividends two years ago. It felt amazing to get $50 in my account from nowhere. Now I get about $200 every quarter.

It’s like having a tiny side job that I don’t work at. The Dividend Investing Calculator shows you how much income you could get from dividend stocks. You can see how dividends add up over years. Many people use this for retirement income. When dividends get paid, you can either spend them or buy more stocks. Buying more stocks is called reinvesting, and it makes your money grow faster.

How Compound Interest Changes Everything

This is where investment calculators get really exciting. Compound interest is the reason why starting early matters so much. Let me explain with a story. My friend Alex started saving $200 per month at age 25. His friend Ben started saving $400 per month at age 35. Who do you think has more money at age 65? Alex does. Even though he saved less per month, he had 10 extra years for his money to grow.

Those 10 years made a huge difference. The calculator shows Alex ends up with about $200,000 more than Ben. This happens because your earnings also earn money. In year one, you earn money on your savings. In year two, you earn money on your savings PLUS money on last year’s earnings.

It keeps building like a snowball. Research from the Investor.gov financial education program shows that compound interest is the most powerful tool for building wealth. You don’t need to be rich. You just need to be patient.

Mobile Apps vs Website Calculators

You can find investment calculators on computers and phones. Both work well, but they’re a bit different. Website calculators usually have more options. You can adjust lots of settings and see detailed charts. I use these when I’m doing serious planning. They’re better for printing and saving your results. Mobile apps are faster and easier.

I have one on my phone that I check while waiting in line at the store. They’re great for quick estimates. Many apps also send you reminders to update your goals. The best approach? Use both. Do your big planning on a computer. Check quick updates on your phone. That’s what I do, and it keeps me on track without taking too much time.

Understanding Investment Risk with Calculators

Risk means the chance that your investments might go down instead of up. Calculators can help you understand this. Safe investments like savings accounts never go down, but they grow very slowly. Risky investments like stocks can grow fast, but they also can lose money.

The trick is finding the right mix for you. Most calculators let you choose different risk levels. Conservative means safe and slow. Moderate means medium risk. Aggressive means higher risk with possible higher rewards. I’m 35, so I use a moderate-aggressive mix. I have time to recover if the market drops. My dad is 68, so he uses a conservative mix.

He can’t afford to lose money this close to retirement. A good rule: the younger you are, the more risk you can take. The older you are, the safer you should play it. Your calculator should match your age and comfort level.

Tax-Advantaged Accounts and Calculators

Some investment accounts give you tax breaks. These special accounts can save you thousands of dollars.

- 401(k) accounts are offered by many jobs. Money goes in before taxes, which means you pay less tax now. Your calculator needs to account for this. If you put in $500 per month, it might only cost you $400 after tax savings.

- Roth IRA accounts work differently. You pay taxes now, but not later. When you’re 65 and withdraw $100,000, you keep all of it. No taxes. This is huge.

- 529 accounts are for college savings. You don’t pay taxes on the money when you use it for education. I’m using one for my nephew.

Regular calculators don’t always show tax benefits. Look for calculators that specifically mention tax-advantaged accounts. They give you more accurate numbers.

Goal-Based Investment Planning

Different goals need different plans. A calculator helps you make a specific plan for each goal. My biggest goal is buying a house. I use a calculator that shows me I need $60,000 for a down payment in five years. That means saving $900 per month.

That’s a lot, so I’m also doing side work to earn extra money. Some people save for their kids’ college. Others save for a dream vacation or starting a business. Each goal needs its own calculator run and its own savings plan. Write down your top three goals. Put them in order of importance. Use a calculator for each one.

Then decide how much of your monthly savings goes to each goal. I split my savings: 60% for my house, 30% for retirement, and 10% for travel. Your split will be different, and that’s perfectly fine. Your goals are yours.

Using Historical Data in Investment Calculations

Looking at past market performance helps you make better guesses about the future. But the past doesn’t guarantee anything. The stock market has gone up about 10% per year on average since 1926, according to historical S&P 500 performance data. But some years it went up 30%, and some years it went down 20%.

That’s why we use averages. Most experts say to plan for 7-8% returns on stocks over long periods. This is lower than the historical average, which gives you a safety cushion. If the market does better, you’ll have extra money. If it does worse, you’re still okay. Bonds have returned about 5% over time.

Savings accounts give about 1-2% now. A mix of different investments usually gives somewhere in the middle. Don’t trust any calculator that promises guaranteed high returns. There are no guarantees in investing. Anyone who tells you otherwise is lying.

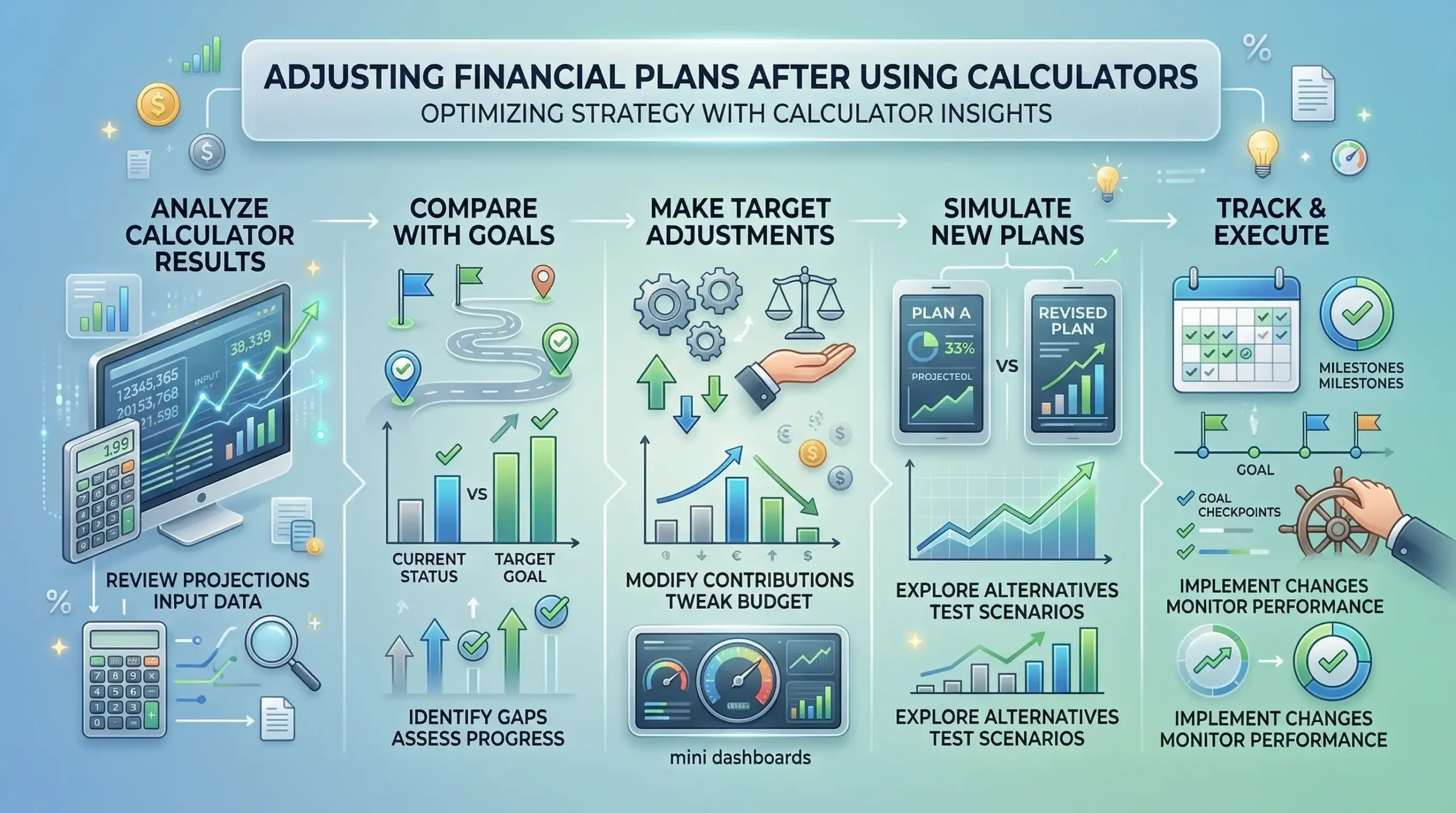

Adjusting Your Plan Based on Calculator Results

The calculator shows you the future, but you might not like what you see. That’s okay. You can change things. When I first used a retirement calculator, it said I’d have way too little money. Instead of giving up, I made changes. I increased my monthly savings by $100. I also started a small side business for extra income. Six months later, I ran the calculator again. Things looked much better. I was on track.

That felt amazing. If your calculator shows you’re short of your goal, you have options. Save more each month, work longer before retiring, or lower your goal a bit. All these work. If your calculator shows you’re ahead of your goal, that’s great! You can either keep the extra cushion or save less and enjoy life more now. I usually keep the cushion because life surprises you.

Why You Should Start Using Calculators Today

Investment calculators cost nothing and take minutes to use. They can save you from huge mistakes and help you reach your dreams. I wish I had started using these tools 10 years earlier. I would have saved thousands more by now. But the best time to start is always today. Pick one goal.

Find a simple calculator. Put in your numbers. See what happens. Then make a plan. That’s all you need to do right now. You don’t need to be perfect. You don’t need to understand everything about finance. You just need to start somewhere. The calculator will guide you from there. Your future self will thank you for taking this step today. Trust me on that.

Conclusion

Investment calculators are powerful tools that anyone can use to plan their financial future.

They help you see clearly where your money is going and what it could become. Whether you’re saving for retirement, your kids’ college, or a big purchase, these calculators show you exactly what you need to do.

Start with the basics. Know your starting amount, monthly savings, time frame, and expected returns. Use simple tools like the Compound Interest Calculator or Future Value Calculator to see your money grow.

Don’t let perfect be the enemy of good. Your first calculation won’t be perfect, and that’s fine. What matters is that you start planning today instead of waiting for tomorrow.

I’ve seen these tools change lives. They changed mine. Now it’s your turn to take control of your financial future.