You’re looking at your house – the place where your kids took their first steps, where you drink coffee every morning, where all your stuff lives. But here’s something that keeps many people awake at night: what if something bad happens? Getting house insurance quotes is the first step to protecting everything you’ve built.

What Are House Insurance Quotes?

A house insurance quote is simply an estimate of how much you’ll pay to protect your home. Think of it like going to three different stores to see which one sells milk for the cheapest price – except you’re shopping for protection, not groceries.

When you ask for a quote, the insurance company looks at your house and tells you, “We can protect your home for this much money per month.” It’s not a final price yet. It’s just their best guess based on what they know about your home.

Why You Need Multiple Quotes

I learned this the hard way when I bought my first house in 2019. I went with the first quote I got because I was tired and just wanted to be done with paperwork. Big mistake. I later found out I was paying $600 more per year than I needed to.

Here’s why you should get at least three quotes:

First, every company looks at risk differently. One company might think your old roof is a big problem. Another might not care as much. Second, companies offer different discounts. You might get a better deal at one place just because you have a burglar alarm. Third, prices change all the time. What was cheap last year might not be cheap this year.

According to a study by the Insurance Information Institute, homeowners who compare at least three quotes save an average of $480 per year. That’s real money you can use for other things.

How Quotes Are Calculated

Insurance companies use a lot of information to figure out your quote. They look at your house like a doctor looks at a patient.

They check how much it would cost to rebuild your home if it burned down tomorrow. This is called replacement cost. They don’t care what you paid for the house. They care about lumber prices, labor costs, and how big your house is.

They also look at risk. Do you live near a fire station? That’s good – your quote goes down. Do you live in an area where hurricanes happen? That’s risky – your quote goes up. They even check your credit score in most states. People with better credit usually get better rates.

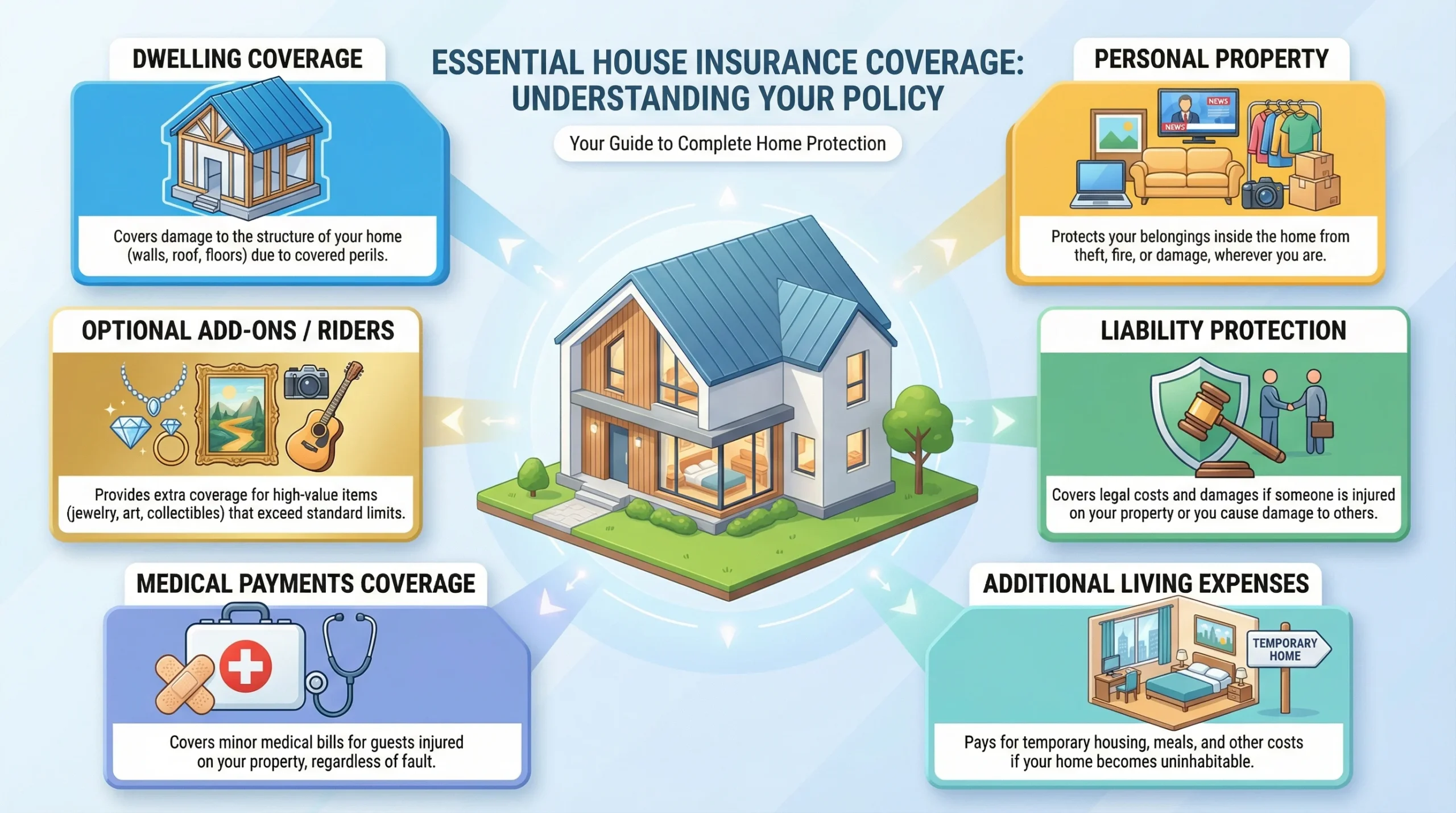

Types of House Insurance Coverage

When you’re looking at house insurance quotes, you need to know what you’re actually buying. It’s not just one big blanket of protection. It’s more like a pizza with different toppings – each part covers something different.

Most policies have six main parts. Let me break them down.

Dwelling Coverage Explained

This covers the actual building you live in. The walls, the roof, the floors – the whole structure. If a tree falls on your house, dwelling coverage pays to fix it. If a fire destroys your kitchen, this coverage helps rebuild it.

The tricky part is figuring out how much coverage you need. I once helped my neighbor after a small kitchen fire. His insurance only covered half the damage because he didn’t have enough dwelling coverage. He had to pay $15,000 out of his own pocket.

Most experts say you should insure your home for at least 80% of what it would cost to rebuild. But honestly? I always recommend 100% or more. Materials and labor get expensive fast, especially after a disaster when everyone needs contractors at the same time.

Your mortgage company will require you to have dwelling coverage at least equal to your loan amount. But that might not be enough. Your loan is based on what you paid for the house. Rebuilding could cost more.

Personal Property Protection

This part covers all your stuff inside the house. Your TV, your clothes, your furniture, your kid’s toys – all of it. If someone breaks in and steals your laptop, personal property coverage helps replace it.

Most policies cover your belongings for 50% to 70% of your dwelling coverage amount. So if your house is insured for $300,000, your stuff might be covered for $150,000 to $210,000. Seems like a lot, right? But walk through your house and add up everything. You might be surprised how fast it adds up.

One thing to watch: there are limits on certain items. Most policies only cover $1,000 to $2,000 for jewelry, no matter how expensive it is. Same with valuable items like art or collectibles. If you have expensive stuff, you need extra coverage called a rider or endorsement.

My friend Sarah learned this when her engagement ring got stolen. The ring cost $8,000, but her insurance policy only paid $2,000 because she didn’t have a jewelry rider. She was heartbroken – not just about losing the ring, but about the money too.

How to Get House Insurance Quotes Online

Getting quotes used to mean calling agents on the phone and answering the same questions over and over. Now it’s much easier. You can get quotes while sitting in your pajamas drinking coffee.

The process usually takes 10 to 15 minutes per company. I recommend setting aside an hour to get three to five quotes. This gives you time to do it carefully without rushing.

What Information You’ll Need

Before you start clicking around for quotes, gather your information first. This saves time and makes sure all your quotes use the same details.

You’ll need your home address, obviously. Then get your property details ready: how many square feet, when it was built, what the roof is made of, and when the roof was last replaced. If you don’t know these things, look at your home inspection report from when you bought the place. Or check your property tax records online.

You’ll also need to know what safety features you have. Do you have smoke detectors? A security system? Fire extinguishers? These can lower your quote. Companies love safety features because they reduce the chance of big claims.

Have your current insurance policy handy if you already have one. This helps you make sure you’re comparing apples to apples. You want the same coverage limits and deductible amounts when you’re looking at different quotes.

According to research from J.D. Power, customers who prepare their information beforehand get more accurate quotes and are more satisfied with their purchase.

Best Places to Compare Quotes

You have three main options for getting quotes. Each has pros and cons.

First, you can go directly to insurance company websites. Companies like State Farm, Allstate, and Progressive all let you get quotes online. The good thing is you’re working with the source. The downside is you have to visit each website separately. That’s a lot of clicking.

Second, you can use comparison websites. These let you enter your information once and get multiple quotes. It’s faster. But be careful – not all comparison sites work with all companies. Some only show certain insurance providers.

Third, you can work with an independent agent. These folks represent multiple companies and can shop around for you. I personally like this option because they can explain the confusing parts and answer questions. But you have to find a good agent, which takes some research.

Whichever way you choose, make sure you’re getting quotes from companies with good ratings. Check their AM Best rating – this shows if they’re financially stable. You want at least an A- rating. A company can offer cheap quotes, but if they go bankrupt when you need them, that’s useless.

Factors That Affect Your House Insurance Quotes

Your quote isn’t pulled out of thin air. Insurance companies use specific things about your house and your life to calculate the price. Some you can control. Some you can’t.

Understanding these factors helps you know if a quote is fair. It also shows you where you might be able to save money.

Your Home’s Age and Condition

Older homes cost more to insure. It’s not personal – it’s just math. An old house has old wiring, old plumbing, and an old roof. Old stuff breaks more often.

I have a friend who bought a beautiful house built in 1920. She loves the character and the hardwood floors. But her insurance quote was 40% higher than her sister’s quote for a newer house in the same neighborhood. That old house came with old-house risks.

The roof age is huge. If your roof is more than 15 years old, expect higher quotes. Some companies won’t even insure you if your roof is over 20 years old. They know an old roof is more likely to leak or get damaged in a storm.

If you’re buying an older house, ask about renovation history. A house built in 1950 but updated in 2020 might get better quotes than a house built in 2000 with no updates. Companies care about actual condition, not just age on paper.

Location and Risk Factors

Where you live matters more than almost anything else. Some locations are just riskier than others.

If you live in Florida or Louisiana, your quotes will be higher because of hurricanes. If you’re in California, wildfires are a concern. In the Midwest, it’s tornadoes and hail. Each region has its own risks, and insurance rates reflect that.

A report from the National Association of Insurance Commissioners shows that coastal properties pay two to three times more than inland properties for the same coverage. Being near water is expensive.

Even within the same city, quotes vary. If you’re five blocks from a fire station, you’ll pay less than someone who’s five miles away. The faster firefighters can get to your house, the less damage a fire will cause. Insurance companies know this.

Crime matters too. Higher crime areas mean higher chance of theft or vandalism. This shows up in your quote. I lived in a neighborhood where car break-ins were common. My quote was $200 higher per year than my friend’s quote in a quieter area nearby.

Average Cost of House Insurance in 2026

Let’s talk money. What should you actually expect to pay for house insurance?

The average American pays about $2,424 per year for house insurance, according to recent data. That’s about $202 per month. But averages don’t tell the whole story. Your cost depends on where you live and how much coverage you need.

To plan ahead, you can use a Future Value Calculator to estimate how your insurance costs may grow over 5, 10, or 20 years

For a home insured for $300,000 in dwelling coverage, you might pay anywhere from $800 to $6,500 per year depending on your state. That’s a huge range.

| Factor | Details | Impact on Insurance |

|---|---|---|

| Home Age & Condition | Older homes (e.g., built in 1920) have old wiring, plumbing, and roofs. Renovations can improve rates. | Older homes cost more to insure. Roofs >15 years old increase quotes; some insurers won’t cover roofs >20 years old. Renovated older homes may get better rates than newer, unrenovated homes. |

| Roof Age | Roofs degrade over time and may leak or be storm-prone. | Major factor in insurance cost; older roofs = higher premiums. |

| Location | State and local risks: hurricanes (FL, LA), wildfires (CA), tornadoes/hail (Midwest). Coastal vs. inland properties differ. Proximity to fire station matters. | Higher-risk locations increase premiums significantly. Being closer to emergency services can reduce rates. |

| Crime | Areas with higher theft or vandalism rates. | Higher crime = higher insurance quotes. |

| Average Cost (2026) | Average US home insurance: $2,424/year (~$202/month). For $300,000 dwelling coverage: $800–$6,500/year depending on location and coverage. | Cost varies widely based on home age, condition, location, and coverage. |

State-by-State Price Differences

Location is everything when it comes to insurance premiums. Let me give you real numbers.

Vermont is the cheapest state for house insurance, with an average of just $827 per year. Delaware and New Hampshire are also cheap, around $966 and $1,039 per year. These states don’t have many hurricanes, earthquakes, or other big natural disasters.

On the other end, Nebraska is expensive at $6,587 per year. Louisiana costs about $6,274 per year. Florida averages $5,838 per year. These states deal with hurricanes, tornadoes, and flooding. More risk means higher prices.

If you plan to offset some of these costs with investments, a dividend calculator can help you estimate potential income to cover yearly insurance premiums.

I moved from Ohio (average $1,364 per year) to Texas (average $3,899 per year) last year. My new house is actually smaller than my old one, but my insurance more than doubled. That’s just Texas – the weather is rougher here.

Understanding your state’s average helps you know if a quote is reasonable. If you’re in Vermont and someone quotes you $3,000 per year, something’s wrong. But in Louisiana? That might actually be a good deal.

How to Lower Your Premium

Good news: you don’t have to accept whatever quote you get. There are real ways to bring that number down.

Bundle your policies. Almost every company offers a discount if you buy your home and car insurance together. I save about $380 per year by bundling. It’s free money just for buying from the same place.

Increase your deductible. This is how much you pay out of pocket before insurance kicks in. If you raise your deductible from $500 to $1,000, your premium might drop 10% to 25%. Just make sure you actually have that money saved in case something happens.

You can calculate how your savings can grow over time to cover higher deductibles using a compound interest calculator with withdrawals.

Install safety devices. A monitored security system can save you 10% to 20%. Smoke detectors, fire extinguishers, and sprinkler systems also help. The safer your house, the less risk for the insurance company.

Improve your credit score. In most states, people with better credit pay less for insurance. It’s weird but true. Companies found that people with good credit file fewer claims. Work on paying bills on time and reducing debt. Your credit score affects more than just loans.

If you invest in stocks to build an emergency fund, a Stock Average Calculator can help you understand your average purchase price and potential gains over time.

Stay claims-free. Every time you file a claim, your rates might go up. If the damage is small – like $1,500 when your deductible is $1,000 – consider just paying for it yourself. Three years with no claims can earn you a claims-free discount.

Ask about other discounts. Are you over 55? Retired? A loyal customer? Some companies offer discounts for these things. My mom got a 10% discount just for being a long-time customer. Never hurts to ask what’s available.

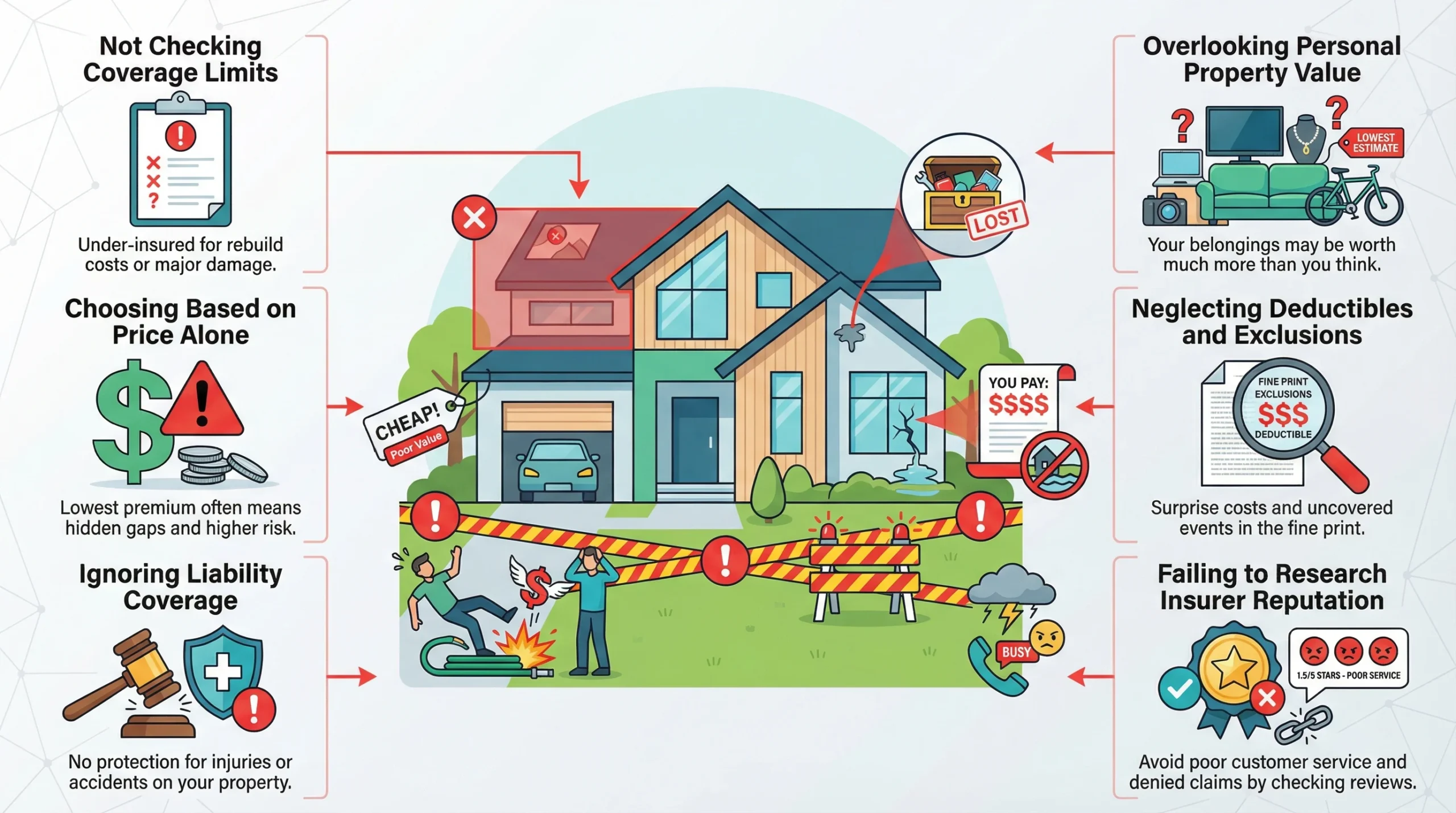

Common Mistakes When Comparing House Insurance Quotes

I’ve seen people make the same mistakes over and over when shopping for house insurance quotes. These mistakes cost real money and cause real problems when disaster strikes.

Let me tell you about my neighbor Tom. He got three quotes, picked the cheapest one, and thought he was done. Smart move, right? Wrong. When a pipe burst and flooded his basement, he discovered his cheap policy didn’t cover water damage from plumbing issues. He paid $12,000 out of pocket.

The truth is, shopping for insurance is more than finding the lowest number. It’s about getting the right protection at a fair price.

Not Checking Coverage Limits

This is the biggest mistake people make. They see “$150,000 in personal property coverage” and think that’s plenty. But they don’t actually calculate what all their stuff is worth.

Walk through your house right now. Think about replacing everything. Your couch, your TV, your clothes, your dishes, your tools, your kids’ stuff, everything in every room. It adds up faster than you think. Most people have way more stuff than they realize.

I made this mistake myself. I thought $100,000 in personal property coverage was more than enough. Then I actually created a home inventory and was shocked. Just our kitchen appliances, furniture, and electronics totaled almost $80,000. And that didn’t count clothes, books, or anything in the garage.

Also check your liability coverage limits. The standard is usually $100,000 or $300,000. But think about it – if someone gets seriously hurt on your property and sues you, medical bills and legal fees can easily hit $500,000 or more. I always recommend at least $500,000 in liability, sometimes even getting an umbrella policy for extra protection.

Choosing Based on Price Alone

Yes, price matters. We all have budgets. But the cheapest quote is often cheap for a reason. Sometimes it’s because the company offers fewer coverages. Sometimes it’s because their customer service is terrible. Sometimes it’s because they deny claims more often.

My friend Jessica learned this lesson. She went with the cheapest quote she could find – $600 per year less than the next option. Then she needed to file a claim after a storm. It took four months to get anyone to respond. Four months of dealing with a damaged roof, calling every day, getting nowhere. The stress wasn’t worth the $600 she saved.

Look at the whole picture. Read reviews. Check the J.D. Power score for customer satisfaction. Look at the AM Best rating for financial strength. A company might be cheap because they’re going out of business.

Also compare the actual coverage details, not just the price. One quote might be cheaper because the deductible is higher. Another might exclude things other policies cover. Make sure you’re comparing the same thing.

Questions to Ask Before Buying House Insurance

Before you hand over your credit card and buy a policy, ask these questions. Seriously. Write them down and ask every company you’re considering.

These questions have saved me from bad policies more than once. They’ll help you too.

What Does My Policy Actually Cover?

Don’t assume anything. Ask specifically about the things that worry you.

Does it cover flood damage? Most standard policies don’t. You need separate flood insurance for that. Does it cover earthquakes? Again, probably not without a separate policy. What about mold? Sewer backup? Dog bites if you have a big dog?

Some companies exclude certain dog breeds. Others limit coverage if your roof is over a certain age. Some won’t cover trampolines or swimming pools without extra coverage.

Get specific answers in writing. Don’t rely on what the agent says on the phone. If it’s important to you, it should be in your policy documents.

Are There Hidden Fees?

Some companies charge policy fees on top of your premium. These can be $50 to $100 per year. Other companies include everything in one price.

Ask about payment fees. Do they charge extra if you pay monthly instead of yearly? Some companies add $5 to $10 per month just for letting you make monthly payments.

What about claim fees? Some policies make you pay an inspection fee before they’ll process your claim. Others include this in your coverage.

Understanding the full cost helps you compare fairly. A quote that seems $200 cheaper might actually cost the same after all the fees.

Conclusion

Getting house insurance quotes doesn’t have to be scary or confusing. Yes, there’s a lot of information to gather. Yes, it takes some time. But protecting your home – your biggest investment and the place where you build your life – is worth it.

Remember these key things: Get at least three quotes. Look at coverage, not just price. Ask questions. Don’t rush. And make sure you understand what you’re buying before you buy it.

The hour or two you spend comparing quotes could save you hundreds or even thousands of dollars. More importantly, it ensures you have the right protection when you need it most.

Your house is more than walls and a roof. It’s where your life happens. Protect it right.